An Effective Business Buyout Tool: a Cash Balance Plan

October 29, 2020Many business owners transitioning into retirement know it can be beneficial when their younger partners choose to buy them out. However, finding a way to finance the buyout can post a significant obstacle for younger partners.

While most aspiring owners may think that buying into a business can only be done with cash or loans, there is another option: a Cash Balance Plan – an innovative, hybrid retirement plan that may provide buyout funding opportunities along with an exit strategy that enables all the parties to benefit.

How a Cash Balance Plan Changes the Dynamic

The money for a buyout has to come from somewhere. But if newer, often younger, prospective owners don’t have the immediate resources needed to buy out exiting (typically older) partners, the deal can reach an impasse.

However, by adding a Cash Balance Plan to an existing 401(k) with a profit-sharing feature, there’s an opportunity to move past the lack of immediate funding. For older partners, who would like to retire in five years or longer, adding a Cash Balance Plan can allow them to make large contributions, often ranging from $150,000 to more than $300,000 annually per partner. This strategy is similar to the old method of a “work‐in” where it was “understood” that a prospective partner worked at a reduced income for a period of time as a way to “pay” the older partners and then become an equity partner.

A Cash Balance Plan Can Help Avoid Higher Taxation

Current tax laws create a taxation dilemma for both the younger owners and the retiring older partners. The younger, prospective owners have to use “after‐tax” dollars (generally from earned income) to fund the buy‐in. At the same time, the older, retiring partners will have to pay higher capital gains tax rates (often as high as a 23.8% federal rate plus state tax) on the sale. This higher capital gain rate can be a large percentage of the sale proceeds, especially if the exiting owner has a low tax basis.

For example, a buy-in payment of $500,000 could “cost” almost $1 million in pre‐tax dollars, especially in high‐income tax states such as Massachusetts, California, and New York. Between the income taxes paid by the buyer on money needed for the sale and the taxes paid by the seller on the proceeds of the transaction, more than half of the buyout cost may be needed for federal and state taxes.

But if the business owners strategically incorporate a Cash Balance Plan, the contributions become a tax‐deductible expense for both the firm and, by extension, the new younger business owner(s). And, on the seller’s side, the deposits are tax‐deferred until the retiring seller starts withdrawing the funds after retirement (and typically after age 72). Until the money is withdrawn, it will be invested and can grow on a tax‐deferred basis over a period of years, and then distributed when the seller is usually in a lower tax bracket.

Depending on the seller’s retirement income tax rate and other sources of income the result could be similar to preferential long‐term capital gain rates. If the tax differential between the rates of tax on earned income versus long term capital gains is more than 7‐10%, then the “sale price” for the retiree’s partnership interest can be increased to offset the difference in tax treatment. The selling partner could either receive more substantial annual contributions to their Cash Balance account over the same period or the same amount for a longer period to make up the difference.

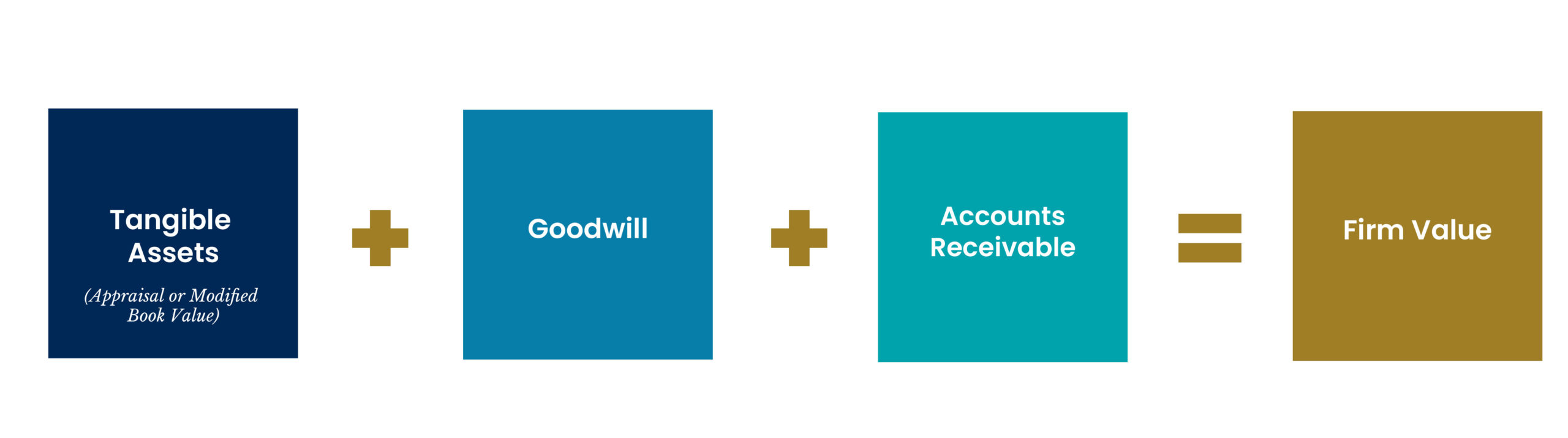

What’s a Business Worth?

There are many ways to design and or determine the value of a business. One method is to have a firm valuation calculated. Typically, this valuation is based on the following components:

While this is just one possible equation, determining the value for the business is the first step in designing a Cash Balance Plan compensation structure that allocates contributions “favoring” the retiring owners. Once the business establishes its value and, therefore, the selling price, then a discussion about how to structure/modify the funding (the terms) of the Cash Balance Plan can be held with the pension actuary and financial advisor. After a probable implementation strategy is validated, a plan is presented to the younger partners.

Let’s imagine a scenario where there’s a significant age difference between the retiring partner and the buying partner. In this case the retiring partner can have much larger annual cash balance contributions than the buying partner. Assuming both partners have the same base W‐2 income, then the pre‐tax Cash Balance contribution can be modified extensively to generate economic benefit to the retiree.

Since the partners set and have control of all the economic variables related to compensation, they can modify and adjust W‐2 compensation, and/or add more or reduce pension benefits for employees, and therefore move their current taxable K‐1 income/profits up or down in order to arrive at the most advantageous economic benefit for the buyout.

It is these levers that need to be adjusted to properly allocate benefits to a retiring practitioner. For example, assume you have an agreed-upon goal of a retiree being willing to end their business ownership and have a buyer take their place as a partner. Let’s assume the goal is $1,000,000 to be accumulated over five years. In this instance, we can calculate the payments needed to be contributed throughout this time period. An annual contribution to the retiring partner’s Cash Balance account of approximately $175,000 earning 6% for the next five years will likely accumulate the desired amount. Assuming the business has the excess cash flow to make these payments, and the entering partner is willing to forego that prospective income for a period of time, this strategy can deliver the desired benefit. Meanwhile, the entire business and its owners will benefit from the tax deduction associated with this and any cash balance contributions.

A Case in Point

Modera oversaw a Cash Balance Plan structure that resulted in total contributions of over $1,000,000 for a single retiring 64-year-old business owner. The contributions were made over three years and were able to “legally discriminate” in favor of the retiree, because of her age and her high pre‐retirement income. (The wording above is specific terminology in the ERISA/Department of Labor regulations for Cash Balance Plans). The retiring partner was then able to hand over the reins to the next generation, lower her workload, ensure continuity, and contribute a significant amount toward her retirement. The younger partners were very willing to delay income increases while taking on more work to ensure the retiring partner received the economic benefits she deserved and earned as a founder of the business.

Does a Cash Balance Plan Make Sense for Your Business?

In the appropriate small business environment, a Cash Balance Plan can offer a tremendous advantage for older business owners. In essence, younger partners are effectively treating the substantial retirement plan contributions to senior partners as installment payments in his or her ownership interest. Until the Cash Balance plan contributions have reached the predetermined buyout contribution amount, both key‐person life insurance and long‐term disability for owners should be considered.

Using a Cash Balance Plan early in the process of planning for older owners’ retirements will reduce the pressure on younger partners who have to come up with sizeable after‐tax lump sums, and the anxiety of older partners who don’t have a clear exit strategy. With some added creditor protections that vary with state/federal law thrown in for good measure, this type of planning could help bring peace of mind and concrete results to both older and younger owners.

As with any complex strategy, individual specifics govern whether or not this strategy will achieve the desired results. Be sure your pension actuary runs scenarios using actual plan participant data to see if implementing the plan makes sense. And keep in mind, such plan design enhancements require plan amendments as well as careful implementation and tracking to ensure alignment with changing business ownership objectives.

Modera Wealth Management, LLC (“Modera”) is an SEC registered investment adviser. SEC registration does not imply any level of skill or training. Modera may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. For information pertaining to Modera’s registration status, its fees and services please contact Modera or refer to the Investment Adviser Public Disclosure Web site (www.adviserinfo.sec.gov) for a copy of our Disclosure Brochure which appears as Part 2A of Form ADV. Please read the Disclosure Brochure carefully before you invest or send money.

This article is limited to the dissemination of general information about Modera’s investment advisory and financial planning services that is not suitable for everyone. Nothing herein should be interpreted or construed as investment advice nor as legal, tax or accounting advice nor as personalized financial planning, tax planning or wealth management advice. For legal, tax and accounting-related matters, we recommend you seek the advice of a qualified attorney or accountant. This article is not a substitute for personalized investment or financial planning from Modera. There is no guarantee that the views and opinions expressed herein will come to pass, and the information herein should not be considered a solicitation to engage in a particular investment or financial planning strategy. The statements and opinions expressed in this article are subject to change without notice based on changes in the law and other conditions.

Investing in the markets involves gains and losses and may not be suitable for all investors. Information herein is subject to change without notice and should not be considered a solicitation to buy or sell any security or to engage in a particular investment or financial planning strategy. Individual client asset allocations and investment strategies differ based on varying degrees of diversification and other factors. Diversification does not guarantee a profit or guarantee against a loss.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, and CFP® (with plaque design) in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.