Oil: Where Can I Get My Free Gas?

May 5, 2020These are certainly unprecedented times: a global pandemic, skyrocketing unemployment here at home, and recently…negative oil prices?

Just saying the words “negative oil prices” defies logic. So, what’s going on with oil?

For the first time in history, West Texas Intermediate (WTI) oil prices dropped below $0/barrel on April 20, 20201. In fact, the oil price crashed that afternoon to nearly minus $40/barrel.

Source: FactSet

A Historical Confluence of Events

“Negative oil prices” is a hard concept to get your head around, for sure. But here’s one way to think about it: If you had a smelly, messy, and useless barrel of oil sitting inside your living room that you could not sell, refine, or even give away because no one else wanted it, how much would you pay someone to remove it from your living room as soon as possible?

On April 20th, that is essentially what happened to oil producers and traders who were holding the May WTI oil futures contract. They literally could not give away their contracted barrels that day, and by the afternoon were willing to pay nearly $40/barrel to avoid taking physical delivery of oil barrels when their May contract expired at the end of the trading session on April 20th.

Now the natural question is, why did this happen?

Due to a sudden and overwhelming collapse in demand, the already oversupplied oil market created a situation where there were not enough buyers or even immediate places to store the enormous glut of crude oil.

By way of backstory, there was a historical confluence of events leading up to the WTI crude oil price collapse on April 20th:

Oil was Oversupplied Due to Record Oil Production in the U.S.: Well before COVID-19, the globe was increasingly flush with oil, as the United States had rapidly grown its own oil production over the last decade (sometimes referred to as the “oil shale revolution”) to become the world’s largest producer of oil. In fact, by the end of 2019, the U.S. was producing 19.5 million barrels per day of crude, as compared to the second-largest global producer, Saudi Arabia, which was producing 11.8 million barrels per day.2 Over time, this growth in U.S. oil supply was contributing to the significant downward pressure on oil prices globally. WTI crude, for example, peaked at a record of $147.27 during July 20083 and had since declined to about $61 by the end of 2019.

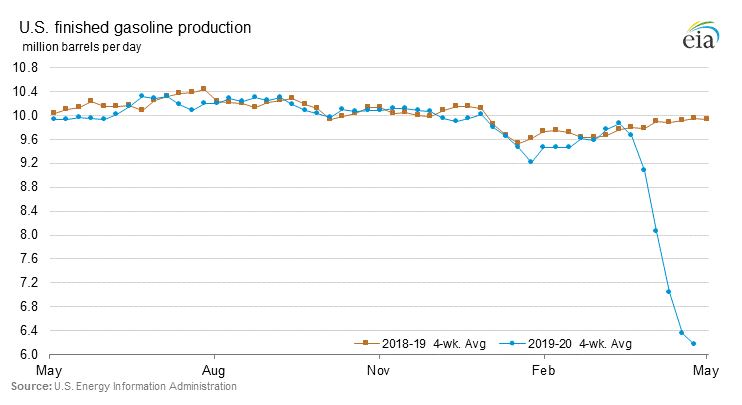

Saudi Arabia-Russia Oil War: Saudi Arabia suddenly increased its oil production to a record 12.3 million barrels a day by early April 2020, in response to Russia’s previous reported unwillingness to coordinate an oil production cut4.Oil Demand Plummeted Due to COVID-19 Pandemic: Demand for gasoline and jet fuel – both of which are consumed products that are refined from crude oil – collapsed with the economic shutdown caused by the COVID-19 pandemic. Gasoline demand in the U.S. during April 2020 was reportedly the lowest level in more than 50 years, and incredibly, down nearly 50% from just a year ago5.

Crude Oil Storage Filled Up: As demand collapsed, more and more produced crude oil was being put into storage. But physical storage options have natural limitations too. Therefore, the oil price collapse on April 20th was a function of the lack of availability and accessibility of crude storage as well.

One ETF Impacted Liquidity of Crude Futures Market: The United States Oil Fund, an exchange-traded fund (ETF) that trades under the ticker USO, is an ETF that attempts to track the price of WTI crude oil by owning WTI futures contracts. As a function of the fund’s objectives, USO had accumulated an estimated 25% of the outstanding May futures contracts for WTI crude during April6.

Unfortunately, ETFs usually simply “roll over” the paper money contracts to the forward month at expiration, and are not designed to ever take physical delivery of crude barrels. This unique scenario resulted in more forced selling of WTI crude on the expiration date of April 20th, at any price.

Does “Negative Oil” Mean Free Gasoline?

Unfortunately, a temporary negative blip in oil prices does not mean free gasoline for everyone!

Here’s why: The negative “spot” price on the front-month May WTI contract on April 20th was likely a short-term event caused by contract expiration. This event did not reflect the continuing future price of the commodity. Future crude oil contracts (also known as the futures curve) are all still positive, meaning producers and traders still expect to be able to sell their crude barrels normally in the future.

This is also important to remember when it comes to gasoline prices: there are a number of additional fixed costs (i.e., not included in the crude oil barrel cost) that are passed on to consumers at the gas pump. This can include things like federal or state gasoline taxes, as well as the cost of transportation to and from refiners and gas stations.

What Happens Now?

The good news is that, as long as oil supply exceeds demand in the current environment, there is reason to believe gasoline prices will continue to come down in the near term.

However, the supply-demand factors discussed above that have been helping gasoline prices come down could start to reverse later this year, for the following reasons:

During April, 23 countries committed to cutting 9.7 million barrels per day from the global oil supply7.

Second, U.S oil production is likely to fall from its prior highs, as some oil companies lower production and face financial distress with the recent oil price collapse.

Finally, on the demand side, fuel demand should bounce back once people globally start to travel again via cars and airplanes.

Therefore, some eventual stabilization and reversal in fuel prices seems likely over time as the oil supply-demand situation comes into better balance.

As much as we would like to see gasoline prices keep falling and remain low indefinitely, higher fuel prices caused by higher demand means we are all returning to some sense of normalcy in our lives again. Net-net, that would be a good outcome.

Modera client portfolios are globally diversified which include investments in energy stocks and bonds. Movement in oil prices is reflected in the market values of your mutual funds and ETFs.

Please contact your Modera Wealth Manager if you have any follow-up questions on this article or regarding your personal financial situation.

https://fortune.com/2020/04/20/oil-prices-negative-crash-price-crude-market/

https://www.eia.gov/tools/faqs/faq.php?id=709&t=6

https://en.wikipedia.org/wiki/Price_of_oil

https://abcnews.go.com/International/wireStory/saudi-arabia-increase-oil-output-record-high-69499304

https://www.forbes.com/sites/rrapier/2020/04/09/gasoline-demand-collapses-to-a-50-year-low/#63a46c1f196e

https://www.bloomberg.com/news/articles/2020-04-17/u-s-oil-fund-to-move-giant-wti-position-as-market-sours

https://www.wsj.com/articles/opec-allies-look-to-resolve-saudi-mexico-standoff-and-seal-broader-oil-deal-11586695794

Modera Wealth Management, LLC (“Modera”) is an SEC registered investment adviser with places of business in Massachusetts, New Jersey, Georgia, North Carolina and Florida. SEC registration does not imply any level of skill or training. Modera may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.

For additional information about Modera, including its registration status, fees and services and/or a copy of our Form ADV Disclosure Brochure, please contact us or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). A full description of the firm’s business operations and service offerings is contained in our Disclosure Brochure which appears as Part 2A of Form ADV. Please read the Disclosure Brochure carefully before you invest or send money.

Investing in the equity and other markets involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered a solicitation to buy or sell any security or to engage in a particular investment or financial planning strategy. Individual client asset allocations and investment strategies differ based on varying degrees of diversification and other factors. Diversification does not guarantee a profit or guarantee against a loss. Not all asset classes or funds discussed herein are held in all Modera client accounts, and the asset classes and indices discussed in this quarterly letter were selected for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell any securities. The performance of Modera client accounts may differ depending upon actual composition.

Modera Wealth Management, LLC (“Modera”) is an SEC registered investment adviser. SEC registration does not imply any level of skill or training. Modera may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. For information pertaining to Modera’s registration status, its fees and services please contact Modera or refer to the Investment Adviser Public Disclosure Web site (www.adviserinfo.sec.gov) for a copy of our Disclosure Brochure which appears as Part 2A of Form ADV. Please read the Disclosure Brochure carefully before you invest or send money.

This article is limited to the dissemination of general information about Modera’s investment advisory and financial planning services that is not suitable for everyone. Nothing herein should be interpreted or construed as investment advice nor as legal, tax or accounting advice nor as personalized financial planning, tax planning or wealth management advice. For legal, tax and accounting-related matters, we recommend you seek the advice of a qualified attorney or accountant. This article is not a substitute for personalized investment or financial planning from Modera. There is no guarantee that the views and opinions expressed herein will come to pass, and the information herein should not be considered a solicitation to engage in a particular investment or financial planning strategy. The statements and opinions expressed in this article are subject to change without notice based on changes in the law and other conditions.

Investing in the markets involves gains and losses and may not be suitable for all investors. Information herein is subject to change without notice and should not be considered a solicitation to buy or sell any security or to engage in a particular investment or financial planning strategy. Individual client asset allocations and investment strategies differ based on varying degrees of diversification and other factors. Diversification does not guarantee a profit or guarantee against a loss.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, and CFP® (with plaque design) in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.